Today is the 150th anniversary of President Abraham Lincoln's Gettysburg Address.

In many ways, we have come a tremendous way since those days. And yet, according to many accounts, racial tensions are at higher

levels than we’ve experienced since the 1960s. Americans killing Americans.

Americans terrorizing Americans. Americans wasting precious energy tearing

America apart.

Wake up, America! We can not afford to be fighting amongst ourselves.

Coincidently, (or not so coincidentally), the Cold War is

alive and well in the mind and actions of Russian President Putin. In fact it’s

more than alive and well – in some ways the Cold War is at even higher levels

than the 1960s. The closest to the U.S. that the Russian military dared to

venture back then was Cuba. Just last week, Putin announced to the world that he plans to

regularly fly warplanes in the Gulf of Mexico.

You must admit, the man has impeccable strategic timing. These days, who’s

going to stop him in the Gulf of Mexico or anywhere else?

Imagine for a moment the worst case scenario. What if some enemy of the U.S. made up fabricated claims about eminent domain or

some other “cause” and decided to “annex” some of our Gulf of Mexico islands as their own? For instance, what if some other country took military

control of South Padre Island, Texas, or a few of the Florida Keys and then threatened to take over the rest of

the state?

We would need to work side by side with every American

citizen we have, regardless of race, gender, sexual orientation, religious

belief, ethnic background, and so on, to defeat the greatest external military incursion we’d had to

face since the founding of our country.

I wonder if we’d be able to get every citizen

working together, side-by-side, in certain regional pockets of our country, in

certain areas of my own state or even in my own city. Thankfully, my city and

state aren’t located along the coast of the Gulf of Mexico and hopefully won’t

be put to the test any time soon.

I never thought I would say this, let alone write it. But in

a way, I hope President Putin follows through on his threats to fly war planes over

the Gulf of Mexico. Flaunt Russia’s military strength in front of us all. Give us an extremely compelling reason

to unify as American citizens. Just don’t hurt anyone.

And, if you’re going to fly by, please conduct your aerial

exercises soon. I’d hate for US to have already killed each other, so there’s

no one left to defend our peace, if you ever decided to attack.

Wake up America!Let’s return our energy and focus to keeping ALL Americans safe and free

to pursue a life of happiness. Isn't that what being an American citizen

is about in the first place?

Peace, love, and hope to all,

Sera Macintosh

P.S. And I certainly hope that were President Putin to

decide to infringe on the territory of our Gulf of Mexico neighbors instead of

US, that we would NOT leave Mexico standing alone in defense of North America’s

borders. Remember: United we stand. Divided we fall.

For Biblical Adam, one bite of the apple cost him Paradise.

As the story goes, Adam's lust dead-ended in shame, with Adam and Eve dressing in fig leaves and exiled from Paradise for the rest of eternity.

Snow White went comatose after her tainted bite.

Fortunately, things aren't quite as harsh for Apple, Inc.'s investors, as it was for Adam and Snow, even though they're being forced to live in a post-Jobs world.

But it may be time to quit biting the apple, regardless. After all, not everyone can expect a Prince Charming awakening from their Apple-induced slumber.

While I'm in the minority with my advice, at least I'm not the only one saying it's time to quit biting.

According to the 3/1/14 Wall Street Journal, just 69% of Wall Street's analysts rate APPL a "Buy," versus 94% in September, 2012. In fact, several institutional investors and major funds are at their lowest levels of Apple stock holdings in 5 years.

The following three signals caused my "Quit Biting the APPL" recommendation, and/or advice to at least begin shedding some of your investment, if you're in too deep for an abrupt exit.

1) To increase Earnings per Share, Apple's manipulating the financial factors that affect EPS and/or share price (stock buyback program, increasing cash dividends), rather than actually increasing earnings or shareholder value.

2) Apple is also, albeit somewhat stealthily, trying to M & A their way out of the creativity void caused by the loss of Steve Jobs. In the past year, they've outspent Google, becoming the top purchaser of tech businesses.

3) Apple's CEO, Tim Cook, and the board of directors believe their best strategy for what to do with the $147 billion in cash they've accumulated is to give the money back to shareholders.

The primary reason I find the above signals so alarming

is they indicate Apple doesn't have another "Next Big Thing" they're

planning to unveil anytime soon.

With Steve Jobs as creative visionary, Apple was a great company

because of their product innovation. They unveiled

products we'd never dreamed of, and yet, instantaneously, could no

longer live without.

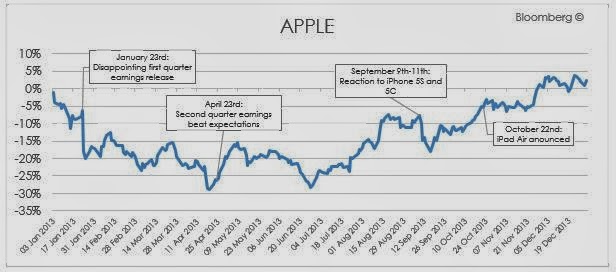

If Apple had another major innovation in the pipeline, like the Macintosh computer, the iPod, iPhone and even iPad - something that'd really change the way we live - they'd need the billions of dollars in cash stockpiles for the massive product launch. If they had such a life-changing invention on the way there's no way their board would be rushing to hand a cash surplus back to shareholders via record dividend payments. And, activist investors like Carl Icahn, wouldn't be demanding cash back, either.

As you can see in the above Bloomberg chart, Apple hasn't had a major innovation (just cool line

extensions) since the launch of the iPad in 2010 - when Steve Jobs was

still alive and kicking!

If the next best device was about about to be unleashed on all of us, Apple wouldn't have to be on such a huge acquisition spree, trying to buy their next greatest invention from outside their company.

Apple's M & A trend concerns me for

several other fundamental reasons. Is Apple, Inc. becoming a tech

holding company? How much experience do they have integrating

acquisitions? Pre-2013, they only did a few small acquisitions here and

there.

Already Tim Cook has the reputation of managing by the numbers (financial statement performance) instead of by the gut - which was his predecessor's purported management style and one that is common among entrepreneurial geniuses.

In my experience, one of the fastest ways to kill creativity in a company is to put the numbers people in charge.

Still, if it weren't for these last concerning developments outlined below, I wouldn't be so strong in my 'Quit Biting the APPL' stance.

I'm not sure what's up, but something doesn't seem quite right in Paradise.

A couple of years ago, Warren Buffett, who doesn't own any Apple stock, publicly recommended to Steve Jobs that Apple should launch a share buy back program, if he thought the stock was undervalued.

Allegedly, Jobs replied that he did consider Apple's stock to be underpriced, but he didn't end up following Buffett's buyback advice.

Post Jobs, in 2013, activist investors, like Carl Icahn, and hedge fund managers like David Einhorn, started demanding Apple do something productive with their massive cash reserves.

So Apple hired Goldman Sachs, (whose major shareholder is Warren Buffett's Berkshire Hathaway investment behemoth), to consult with their board to determine the best strategy for using Apple's $147 billion in cash reserves.

The following 'brilliant' financial strategy emerged as a result:

1) Launch a stock buyback plan. This maneuver boosts earnings per share because there are less shares outstanding over which to spread the company's earnings.

2) Return cash to shareholders via aggressive dividends. The increase in dividends will hopefully allow APPL to maintain its position in the portfolios of the major pension funds and institutional investors that own the majority of Apple's stock.

So far, so good - at least on paper. But here's what really bugs me:

For some unexplained reason, even though Apple's stock buybacks and dividend increases are allegedly about proactively reducing the company's $147 billion cash stockpile, Apple floated a record bond offer of $17 billion.

If Apple was doing the dividend increase and stock buyback program because it has so much excess cash, as the party line would have us believe, why borrow money (via the bond offering) to fund the payouts?

This sounds like something an investment bank would do - NOT a technology rock star!

So, other than generating a bigger paycheck to Goldman Sachs for their management of the bond offering, in addition to their board advisory services, what was the point?

I don't know the answer to my questions. But, I do remember the fundamentals I learned in grad school, while earning my MBA, decades ago:

1) Borrowing cash to pay shareholders' dividends is a classic financial game played by companies in decline who're looking to prop up their share price;

2) Regardless of the amount of cash on hand, borrowing money usually signifies an anticipated cashflow shortfall on the horizon; and

3) Using stock buyback plans as a 'best use of cash' strategy often means one or more of the following effects exist caused by corporate conglomerate malaise taking over a once innovative company - driving it down from great to good.

The company has no better ideas about what it could be developing, producing, or creating with the cash - therefore, there are better investments elsewhere and they're returning the cash/capital to their investors to let them spend it elsewhere.

The company hopes to trigger short-term stock price increases by boosting Earnings per Share via spreading the same earnings over less outstanding shares, rather than actually increasing earnings to boost EPS numbers.

I guess there's nothing wrong with settling for good, especially if you doubt your ability to be great. However, the problem with APPL's share price is that it's still priced for greatness, and the company is no longer as well-poised to deliver it. Although their stock didn't really take a major hit when Steve Jobs died, the loss of his creative genius did cause a huge void right at the core of Apple, Inc. In nature, any apple without it's core will eventually rot and cave in on itself. The same will be true for this corporate powerhouse unless it finds a way to fill the void with a new creative lifeline, and do it quickly.

I do agree the entrepreneurial talent acquisition spree Apple has been on is probably their best bet to fill the void.

It's simply that any M & A strategy is just that - a pretty expensive, unproven gamble.

Take my advice: Quit Biting and/or divest yourself of the APPL. Consider it to be 'Giving up something for Lent," even if you're not Catholic.

Plus, if you shift your investment elsewhere, you're bound to find a tastier choice . . .

Which is not that hard to do, given APPL's stock only appreciated 2% in 2013.

Your new investment choice could be one you'd never have found

If you kept on biting the same old overpriced Apple everyone else is still chewing on.

In closing, here's an oldie but a goodie, from the old Apple Records - The Beatles live, performing "I'm Looking Through You." Thank God for YouTube!

Wanna Make 'Em Pay, But Don't Have Enough Dough to Play? I hope my post from yesterday launches several of you on your way to a bigger 2014 payday, especially if it comes from shorting Berkshire's stock.

If you'd love to make 'em pay, (the financial titans responsible for the global financial crisis most of us are still recovering from), but don't have enough dough to play, as I recommended doing yesterday, U2's got another way.

If you want to have some fun making them pay, just by clicking away, you can, but you have to join me by midnight--and that's Eastern Standard time, my friends.

The "Make 'em Pay" fun continues due to U2 's release of their new song "Invisible." Not only is the song available as a free Invisible iTunes download, but it's better than free because every time the song is downloaded before midnight, tonight, Bank of America has promised to give one dollar for each downloaded track to (RED), the organization Bono cofounded in 2006 to help fight AIDS.

In total, the bank is expected to contribute about $8 to $10 million through 11:59 p.m. EST Monday night to (RED)'s charitable recipient, the Global Fund to Fight AIDS, Tuberculosis and Malaria. The Global Fund provides HIV and AIDS treatment, as well as testing and prevention services, to people in the world's poorest countries. (RED) estimated that it would be able to raise up to $10 million from its partnership with Bank of America.

"We're taking all the energy around the Super Bowl and interest in what U2's doing and flipping it into the fight against HIV AIDS," Bono told USA Todayrecently. He also said that the track, which, according to Rolling Stone Magazine "Bursts with optimism as Bono sings about unity in a relationship," is "sort of a sneak preview – to remind people we exist."

Way to go, Bono and Brian Moynihan, (CEO of Bank of America who took over the reigns after his financial crisis predecessor stepped down).

Not only do I applaud the move, on many levels, but I get to feature two of my favorite Irishmen in the same blog post!

If Not, Maybe You

Should Learn to Read Between the Lines . . .

Didn't you receive your

2013 pay raise? You know, like the 74% increase to $20 million

that Jamie Dimon, king of JP Morgan Chase just received?

Sure it was a tough year, with the U.S. government demanding

a record $20 billion in sanctions against J.P. Morgan Chase for their role in

the 2008/2009 financial crisis and London Whale debacle, but they’re lucky to

have Jamie Dimon, right?

And, even with that awesome pay raise, Jamie’s still

trailing the only other financial-titan-still-left-standing from the financial

crisis years—Lloyd Blankfein.

Yep, Mr. Blankfein, longtime CEO of Goldman Sachs

Group Inc., earned $23 million in salary for 2013, which was only a 9.5% raise

over 2012. Still, nothing to sneeze at!

So if these guys are doing so well, after causing a global

financial crisis less than five years ago, where are the pay raises for the

rest of us? After all, we’re the ones (U.S. and global taxpayers) that bailed

out these kingpins and their crippled financial institutions after they caused

a mess that was way over their collective royal heads.

If you didn’t receive a

sizable 2013 pay raise, you’re probably not using the same strategies as Jamie

Dimon and Lloyd Blankfein. Here’s a few things you may consider doing differently in

2014.

Pay Raise Strategy #1 – Sell a Piece

of Your Hide to Warren Buffett

That’s right,

probably the surest way to guarantee yourself a mega pay raise in 2014 is to

sell a piece of yourself to Warren Buffett.

Following the lead of Dimon and Blankfein, you can commit some pretty heinous financial sins

– if you have Mr. Buffett as your buddy. The problem is this; Warren doesn’t

just buddy up to anybody, he’s usually only interested in you if he owns a

piece of your hide.

The Oracle

of Omaha, through his Berkshire Hathaway empire, has long been a major financier

of Goldman Sachs and lent them billions in the financial crisis.There’s no way Mr. Blankfein would be making $23

million if Buffett didn’t back it—especially in a year when Goldman had flat

revenue and a decline in overall compensation for all the rest of the staffers

at the firm.

And, the

billionaire investor went so far as to call his buddy, Jaime Dimon, “a

bargain.” Because Warren holds his shares in JP Morgan Chase personally,

instead of through his Berkshire portfolio, no one’s sure how much of Jamie’s

hide he owns. But, he sure did go to bat for his buddy Jamie’s, raise, according

to the January 24, 2014 Wall Street

Journal article. “If I owned J.P. Morgan Chase,” Buffett declared, “he

(Jamie Dimon) would be running it, and he would be making more money than the

directors are paying him. . . .If Jamie decides he wants to make more money,

all he has to do is call me and I’d hire him at Berkshire.”

However, if you don’t

think Warren Buffett’s going to be making an offer to buy a chunk of your hide

anytime soon, I suggest learning to read between the lines to secure a pay increase for 2014.

Pay Raise Strategy #2 – Learn To Read

Between The Lines

One of the reasons investment bankers make tons more money

than average folk is that they have entire departments of people devoted to

reading between the lines on their behalf.

So, given it’s the time of the season for annual earnings

releases, I’m going to share with you a few tricks of the accounting trade to

help you “read between the lines” as the major corporations make their 2013

earnings announcements. Hopefully these “Tricks of the Trade” tips will help

you give yourself a

pay raise without anyone but the IRS having to know about it.

Read Between the Lines – Trick #1:

Paper Losses, Now, Ensure Future Profits

If you want

to see a healthy return in your investment portfolio in the near-term (1 – 3 years),

buy

stocks of companies increasing their loss/future cost reserves. For the

most part, reserve increases are paper losses generated by recording more

expense in the current period, which makes it easier to show big profit gains

in future, usually near-term periods. Or conversely, sell stocks of companies where

reserve reductions account for a substantial portion of their current reported

earnings.

The best run

companies, financially, use every opportunity to increase reserves – economic

downturns, acquisitions, global warming, you name it. Another opportune time to

reserve-build to ensure future profits, is when a new CEO or CFO takes the helm

of a major public company. Not only is it a once-in-a-lifetime opportunity to

blame everything on the prior regime, but recording a large loss, or

substantially less-than-Wall Street analyst-expected profit, drives the value

of the new CEO/CFO’s stock options way down, virtually ensuring the options

will increase in value rapidly over the course of the new executive’s reign. A

great example of this is Royal Dutch Shell PLC (Shell Oil).

Royal Dutch Shell PLC – Hides It Well: According to 1/18/14 The Wall

Street Journal, Royal Dutch Shell PLC’s shares fell .9% following their announcement of a profit warning for 2013 earnings. The profit

warning was so rare for Shell, the announcement made

the front page of the Business & Finance section, with the title, “Shell

Bruised by Big Bets- Oil Giant Warns of Rare Profit Miss; New CEO Must Find

Ways to Lift Output.”

Hello! With key phrases like “rare profit miss” and

“new CEO,” in the same sentence, it’s a major signal that some accounting

tricks of the trade may’ve been deployed.

Reading further in the WSJ

article, here are the Read-Between-The-Lines “buy” signs I spotted in Shell

Oil’s “profit-warning” disclosure.

The new CEO, Ben van Beurden, took over the helm

of the company three weeks before the rare “profit warning” was issued. Yet,

he’s no newcomer to the business, as he’s been climbing the ranks at Shell for

years.

Shell hadn’t issued a profit-warning in ten

years. It is a “no surprises,” tightly managed, steady financial performer, in

an industry where price volatility, natural disasters and other major

production interruptions are a constant. They obviously mastered the reserve

game in both their oil and financial operations a long time ago.

It’s important to point out also that the

“profit warning” and “profit miss” don’t mean that Shell’s losing money—they’re

still reporting billions of dollars in profits. Those terms mean that Shell is

“warning” Wall Street’s financial analysts that their profit will “miss” the

analysts’ expectations of what Shell’s profit should be.

The Largest Losses are Paper Ones—Being

Driven By Accounting Entries That Increase 2013 Expenses by Decreasing the Book

Value of Assets or Increasing the Book Value of Reserves:

Included in the $5 billion shortfall from 2012

Q4 earnings, are significant Q4, 2013, asset write-down charges, including a $2

billion write-down of North American shale assets. They’re not writing

these assets down because they’re not producing, they’re just saying “we paid

too much” which in accounting lingo translates to substantially lower

amortization charges in future years, resulting in higher profits from the

exact same assets.

Shell also disclosed its profit warning was based upon “a cost of supplies basis that factors out the impact of inventories.” In

accounting lingo, this means that they’ve given zero value to their own refining

processes or gasoline sitting in their own gas pumps. So regardless of the stage of refining their oil is at,

they’re valuing it in their 2013 financial statements as if it was only in the

raw material state. This way, later on when they recognize the sales of the

2013 end-of-year inventory, they’ll be able to reflect higher margins, because

the inventory (asset) is being carried at a lower-than-market value on their

financial statements.

And, Shell's been outspending its competitors for

the past decade on large capital projects, as they lead the industry in

investment in the perpetual search to find new sources of oil to replenish those

currently being depleted. And in 2013, they’re recording net capital

spending costs of $44.3 billion, up nearly 50% over 2012.

While Mr. van

Beurden is publicly decrying his predecessor’s strategy of funding “elephant

projects,” it’s his term at the helm that’ll reap the benefits of these massive

exploration projects—with as much of the costs of development shouldered by the

prior regime as possible.

Yep, my bet is Mr. van Beurden’s built enough financial

reserves at the end of 2013 to buy himself a nice honeymoon performance for at

least the couple of years. All things being relatively equal, Royal

Dutch Shell’s 2014 profits have got to be much higher than 2013’s. Might as

well buy some shares and take a profitable ride on van Beurden’s back!

Read Between the Lines – Trick #2 – Short Sell the Stock, When

They’re Laying on the Hype

When large

corporations use statistical maneuvers and publicity to divert attention from less

than expected performance, and the stock market seems to believe the hype, even

if the company is still recording billions of dollars in profit, it’s time to “short,”

the stock. The stumble, or even bigger tumble, is definitely

forthcoming—it’s just a matter of when.Senior corporate executives resort to these measures to secure current

year stock option prices and bonuses based on stock prices, trying to maximize

their own paychecks, before the public finds out about whatever they’re trying

to hide.

The

way you get your pay raise for reading between the lines on this one, is to

lock in your “short” price before the financial institutions initiate their own

sell-off. Don’t be greedy or you may not receive your pay day. Just

short the stock at 10% to 20% less than its current price and then tread water

until it’s time to collect your paycheck.

Guess what—the

billionaire investor, buddy of the financial titans, Warren Buffett and his

Fortune 100 conglomerate, Berkshire Hathaway, are providing a perfect example

of where the positive hype doesn’t align with the less than expected financial

results.And, given his backing of the

financial titans’ pay raises, Mr. Buffett’s hype-bubble isn’t about to be burst

open by JP Morgan Chase’s or Goldman Sachs’ analysts in the short-term, so you

still have time to secure your position.

Berkshire

Hathaway – Beware When Warren Buffett Passes the Blame or Tries to Hide the

Shame:

The pre-earnings release hype emanating from Berkshire

Hathaway, Inc., is that Todd Combs and Ted Weschler are tea-leaf readers

extraordinaire—“Better than Buffet”!

Todd Combs Hard at Work

The January 18 - 19,

2014 Wall Street Journal ran an

article entitled, “Buffett Managers Outpace the Boss.” The caption above the

photos of Todd and Ted declared “New Oracles: Berkshire Stock Pickers Shine.”

And, in case readers are dumber than a box of rocks and may’ve still missed the

intended message, below the photos of the two new gurus was the statement, “Two

Berkshire Hathaway managers seen as potential successors to Warren Buffett have

netted better returns than the noted investor.”

It isn’t until the fifth paragraph of the Wall Street’s article that it’s

disclosed, “Mr. Buffett fell short of his own performance target for the

conglomerate for the first time since the Omaha, Neb., native took control of

Berkshire in 1965.”

Even oracles can't be right all of the time!

The next two paragraphs blame Mr. Buffett’s shortfall

performance on the strong stock market, stating, “Thanks to the index’s robust

gains in 2013, Mr. Buffett will fall short of that (his) goal,” and predict Berkshire’s

shareholders aren’t likely to hold the less than expected performance against

Mr. Buffett.

Ted Weschler's Working Hard Too

Four more paragraphs about how wonderful the newly anointed

ones, messers Combs and Weschler, are performing, including this quote from the

Oracle of Omaha, himself, “They’ll both be huge assets for decades to come.”

(Read between the lines – “See, I’ve hired awesome successors, so even though

I’m 83, fear not and buy my stock.”)

Finally in paragraphs twelve and fourteen, there’s a taste

of the pre-Rupert-Murdoch-owned Wall

Street Journal journalistic

skepticism that’s been slowly disappearing from our profit-hungry media these

days.It’s disclosed that each of the

oracles-in-training managed $3 billion in assets, while Warren managed over

$100 billion. In fact, in the final paragraph of the article,

paragraph twenty-two, it’s finally disclosed that the portion of Berkshire's investment

portfolio managed by Mr. Buffett has performed about 38% worse than the S&P 500 over the past five

years.

So

far, there’s been no noticeable hit to the stock price, as most people

are following instructions and “aren’t likely to hold the less than expected

performance against Mr. Buffett.”And,

the mega financial institutions, headed by the likes of Jamie Dimon and Lloyd

Blankfein, wouldn’t dare anger their buddy Buffet by publishing a “Sell”

recommendation for Berkshire’s stock just yet. This means there’s time for you

to lock in your “short sell” position.

The tone of the recent

Wall Street Journal article certainly implied a “buy” or “hold” recommendation,

pointing out that Berkshire’s shares are up 30% over the prior year. However, the

article fails to mention that the S&P 500 was also up 30% over 2012. In

comparison, over at Dimonland, J.P. Morgan Chase’s shares were up 33%, beating

Buffett’s Berkshire and the S&P 500’s performance, despite the record $20

billion in federal sanctions levied against their firm.

Reading between the lines, my tea leaves indicate a “short”

recommendation.

Mr. Buffet and his minions are trying way too hard to make us

believe his heir-apparents outperforming him statistically is the same as them

outperforming him, or the S&P 500, in real dollars.

I don’t know what Mr. Buffett does or does not know about

Berkshire’s performance outlook, but it’s not like the Oracle of Omaha to deflect

the attention away from his own investment portfolio performance or to blame

the S&P 500 for his shortfalls. But, I do know this, real dollars are required to

pay stockholders’ dividends, and over the past five years, Berkshire’s stockholders

would’ve been nearly 40% better off with their real dollars invested in an

S&P 500 index fund.

With that kind of abysmal performance, even Jamie Dimon and

Lloyd Blankfein won’t be able to keep the pension funds and other major

institutional investors drinking Berkshire’s Koolaid forever.

Take my advice, short Berkshire’s stock.Maybe it’ll go viral.

Perhaps the market-trading computer programs will catch on and cause a massive sell-off

in Buffett’s flagship that catches Jamie Dimon, Lloyd Blankfein and the

analysts at J.P. Morgan Chase and Goldman Sachs by surprise and they all lose

money.

Wouldn’t that be great fun, garnering our own 2014 pay raises at the

expense of the very guys who caused our property values to tank, our 401K plans to

plummet, and our jobs to pay less or be cut completely?

In closing, compliments of YouTube, here’s a live performance

off Bonobo’s Days to Come album—the song

“Between the Lines.” As the lyrics so rightly state,

“Things aren't always how they seem

We've got to make the best of it

Eye for an eye

Tooth for a tooth

Sometimes we're blind

We can still see the truth”